Agentic Wallets - When AI Agents Need to Pay

#ai

#web3

AI agents are no longer just answering questions. They are booking flights, managing infrastructure, negotiating with APIs, and completing tasks that used to require a human at every step. But as agents become more autonomous, a fundamental question arises: how does an AI agent pay for things?

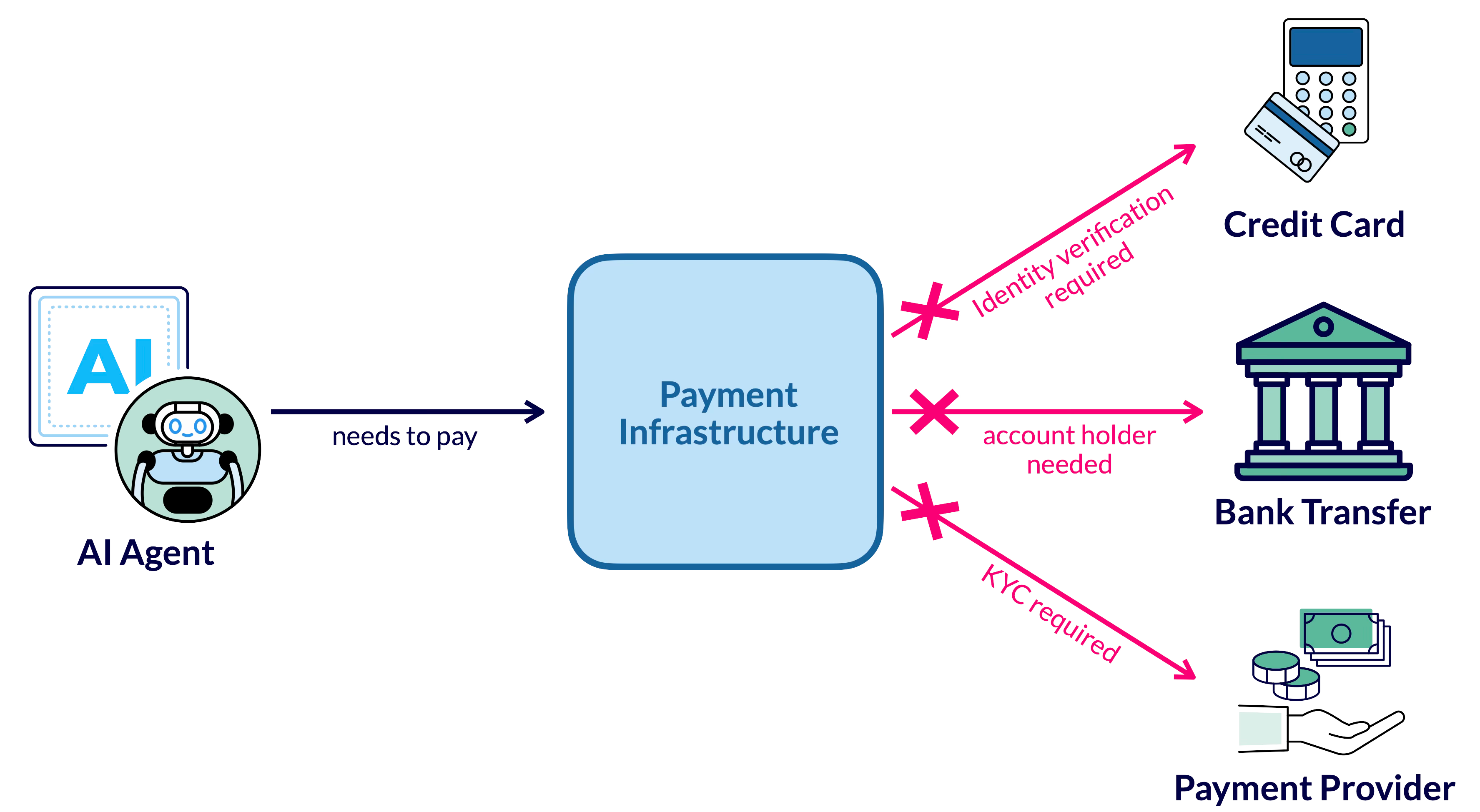

The Problem: Agents Cannot Use Credit Cards

Today's payment infrastructure is built for humans. Credit cards require identity verification, bank transfers need account holders, and payment providers enforce KYC (Know Your Customer) regulations. None of this works well when the "customer" is an autonomous software agent acting on behalf of a user or organization.

AI agents are blocked by traditional payment infrastructure that requires human identity verification

Imagine an AI agent that manages your cloud infrastructure. It detects a traffic spike and needs to spin up additional compute resources from a different provider. Or consider an agent that monitors prices across suppliers and should autonomously purchase materials when the price drops below a threshold. In both cases, the agent needs a way to transact value — quickly, programmatically, and without a human approving every single payment.

This is where the concept of agentic wallets comes in: digital wallets that an AI agent can control — within defined boundaries — to send and receive payments. The idea is not to give agents unlimited financial freedom. Instead, agentic wallets operate under policy-based constraints: maximum transaction amounts, whitelisted recipients, time-based budgets, and human override mechanisms. Think of it like giving an employee a corporate credit card with a spending limit — except the employee is an AI agent.

The Building Blocks: Specifications that exist today

Before diving into wallet architecture and ideas about agentic wallets, we need to understand the emerging specifications that provide the foundation. Two protocols are particularly relevant for agentic commerce since they already define specifications AI agents can interact with.

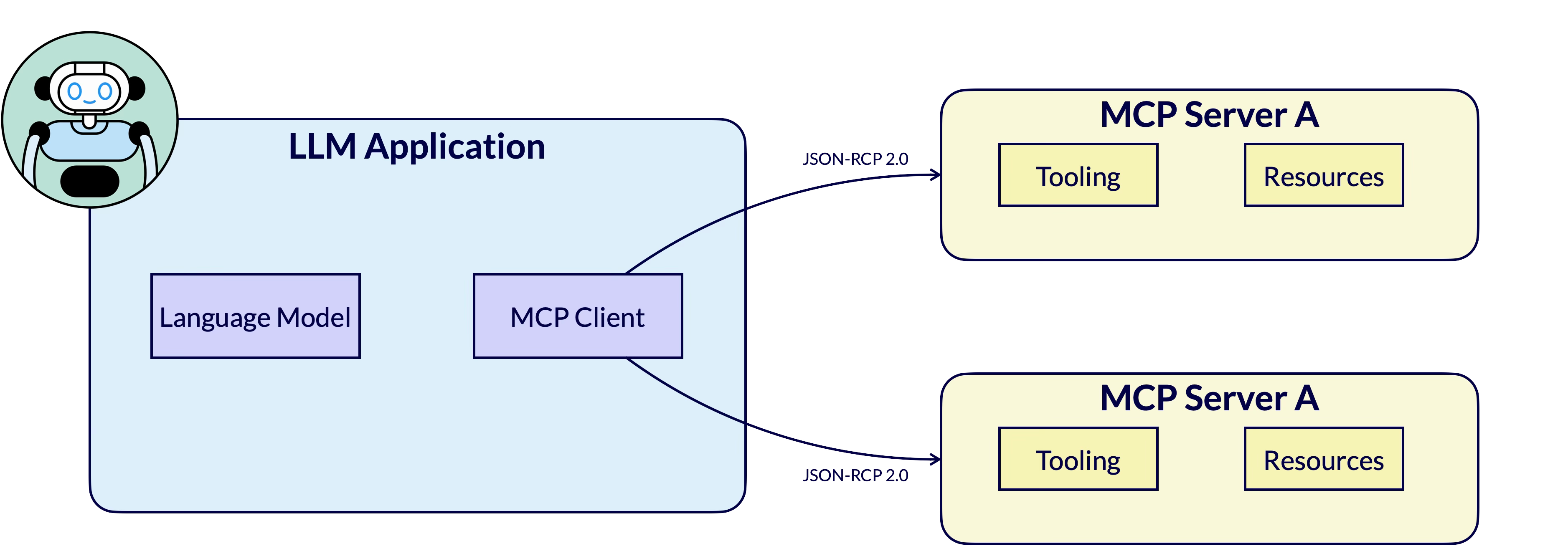

MCP — How Agents Talk to Tools

The Model Context Protocol (MCP) is an open specification that defines how AI agents connect to external tools and data sources. It has originally been created by Anthropic and is now under the Agentic AI Foundation (AAIF) at the Linux Foundation.

MCP architecture:an LLM application connects to multiple MCP servers that provide tools and resources

MCP uses JSON-RPC 2.0 and follows a client-server model: the AI application (host) connects to MCP servers that expose tools (executable functions) and resources (contextual data). When an agent needs to interact with an external service it does not call the API of that service directly. Instead it calls tools on an MCP server that handles the service specific calls.

For agentic wallets, MCP is the communication channel between the agent and the payment infrastructure.

A "Hedera MCP Server" or "Coinbase MCP Server" would expose tools like pay(amount, recipient) that the agent can call without knowing the details of the underlying ledger or payment system.

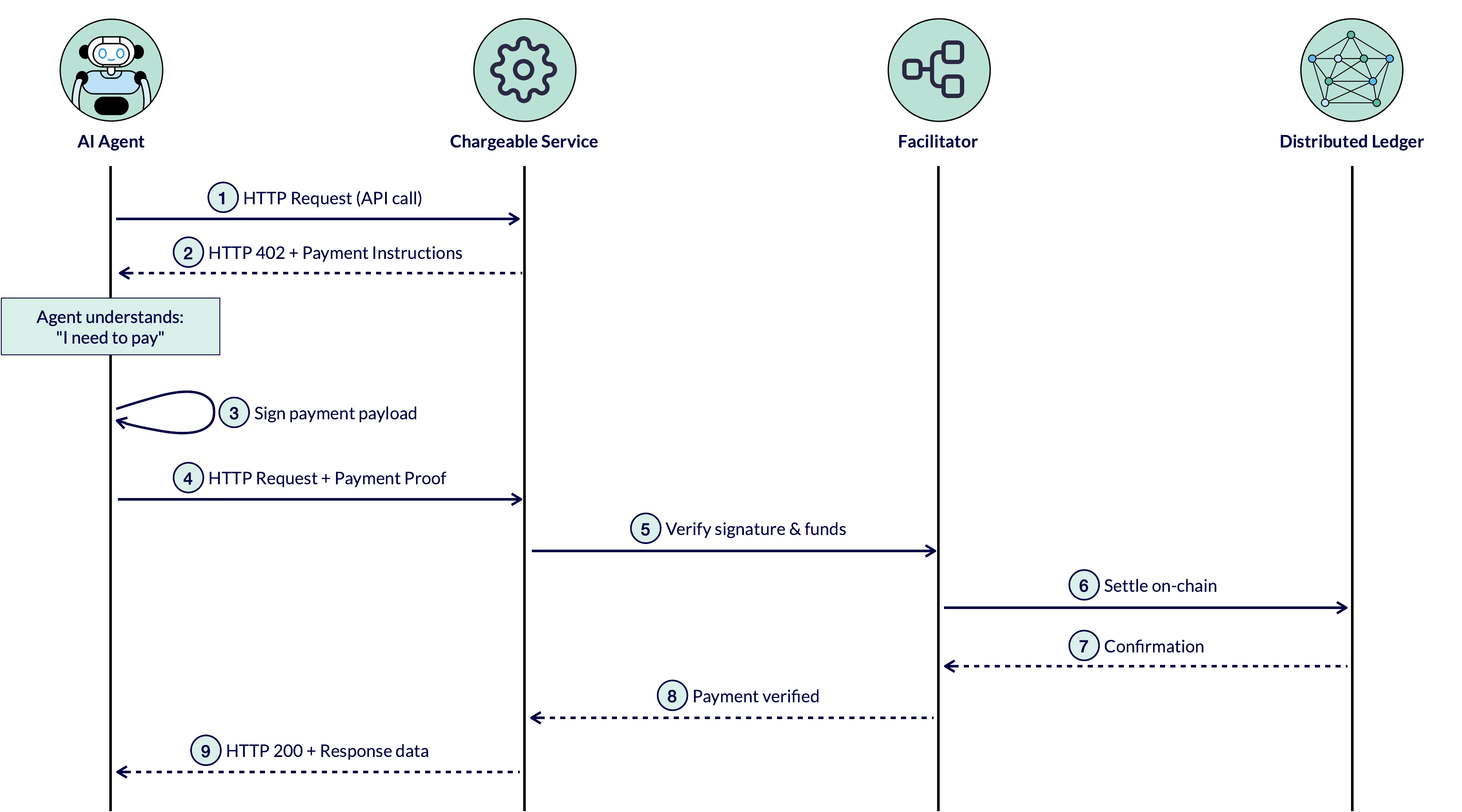

x402 — How Services Signal "You Need to Pay"

x402 is an open payment specification that embeds payments directly into HTTP. The x402 spec is owned by Coinbase. It revives the long-dormant HTTP 402 "Payment Required" status code and turns it into a fully functional payment protocol.

x402 flow: agent calls service, gets HTTP 402 with payment instructions, pays, and retries the request

The flow is simple and elegant:

- An agent calls a service via HTTP

- The service responds with HTTP 402 and payment instructions

- The agent signs a payment payload

- The agent retries the request with the payment proof

- A facilitator verifies the payment and settles it on-chain

- The service delivers the response

No accounts, no API keys, no checkout flows. The agent learns it needs to pay through a standard HTTP response and handles payment programmatically. x402 currently supports stablecoin payments across multiple networks, with over 35 million transactions processed.

For agentic wallets, x402 is the discovery mechanism: the way an agent learns that a service costs money and how much.

My Proposal for Agentic Wallets

As a member of the AAIF working groups I am actively working on exactly these topics. Currently, I'm part of the "Agentic Commerce" and "Agentic Identity & Trust" working groups. By studying the current specifications and approaches in those spaces, I have developed an idea for how agentic wallets could be implemented in a provider-agnostic way. I want to be transparent: I am still learning in this area and do not claim to have all the answers. I would be grateful for any feedback on this proposal — it is meant as a starting point for discussion, not a final design.

The Key Insight: Payment must always be possible

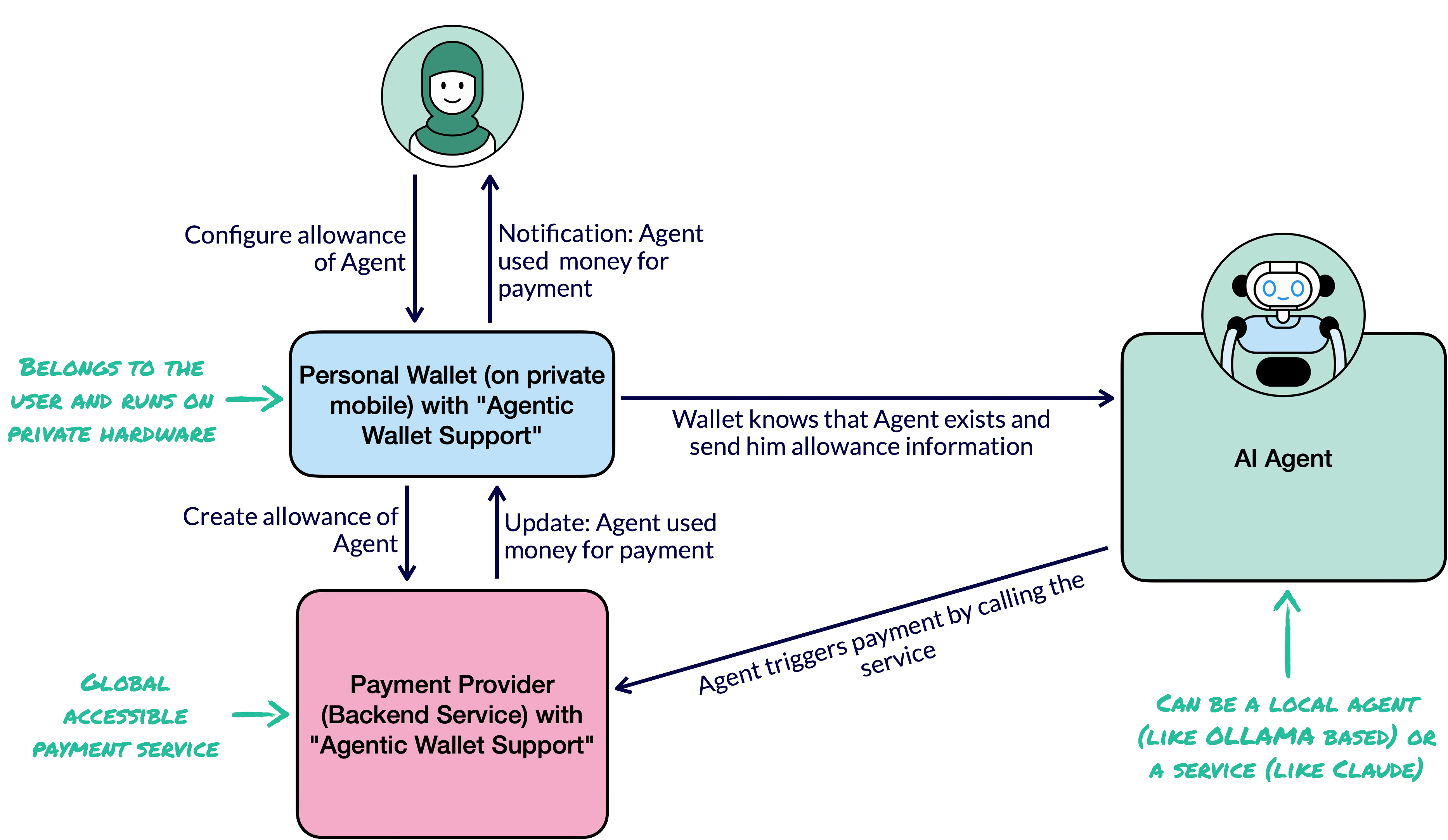

If an AI should autonomously pay for things, the components that are needed for a payment must be always available. We need to give the agent a reliable, always-available payment endpoint with policy enforcement — while the human only needs to be involved for setup and oversight.

The first challenge is where the wallet lives for this use case. In a classical wallet like MetaMask, the user's device holds the private key and signs every transaction. But for agentic wallets, we do not want a personal device to be always online and reachable — that would be a significant security risk. A permanently exposed wallet becomes an attack vector: the device and the private key it holds are targets for remote exploitation, key extraction, or side-channel attacks. Next to that if it runs on your local machine, it must be reachable 24/7. That is unrealistic for mostly all users even if it runs on a mobile device. If it fully runs as a hosted service (e.g., Coinbase), you hand over control to an intermediary.

Based on all that we need a new architecture that allows the user to have full control but do all interactions without the need of a personal device being in the loop.

The client side of an agentic wallet is reduced to what it should be: a configuration and monitoring interface where the human sets policies, approves budgets, and reviews activity. It does not need to be online when the agent transacts, and it does not hold the keys that authorize payments.

Crucially, the human always retains full control. Through the wallet interface, the user can at any time revoke an agent's access, withdraw remaining funds, or reduce the spending limit — regardless of whether the backend is a smart contract or a centralized service.

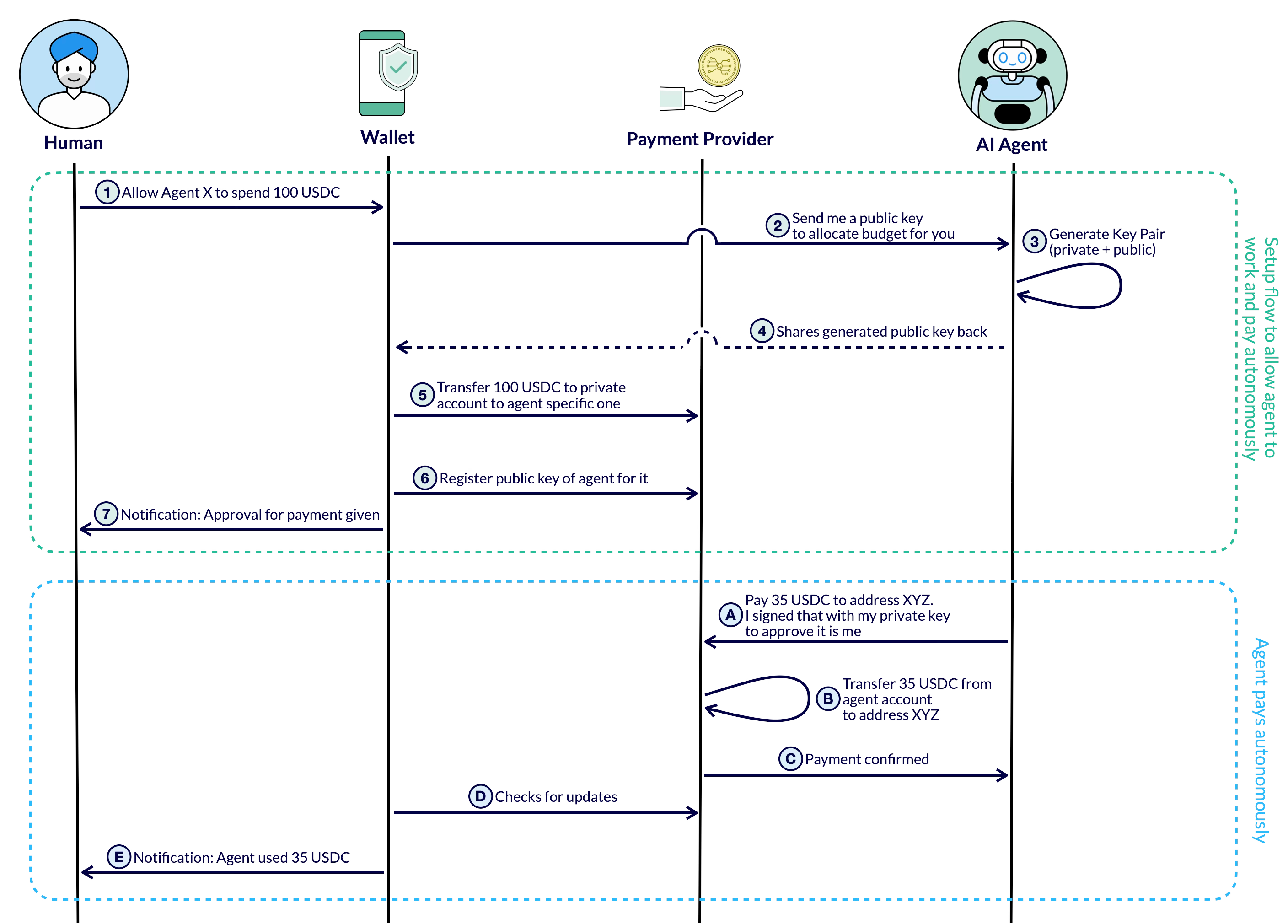

The following diagram shows a very basic idea of how an agentic wallet could work:

Base structure of an agentic wallet payment flow

The Flow of Agentic Wallet Payment

Let's define a concrete flow for an agentic wallet that allows an AI agent to spend money on behalf of a user. My idea how that can be done in a secure and controlable way is by using a private & public key based approach. Here the agent generates its own key pair and the payment provider only needs to know the public key. The agent can then use its private key to sign transactions and the payment provider can verify the signature.

Here is the complete flow for setting up and using an agentic wallet:

Setup phase:

- 1.) The human tells the wallet app: "Allow Agent X to spend 100 USDC on my behalf." Here the wallet already know how to contact the agent or the user needs to add access information.

- 2.) The wallet app contacts the agent and requests its public key. Today no spec exists that defines how the wallet interacts with the agent (as far as I know)

- 3.) The agent generates its own key pair (private + public) that is only used for the given specific payment approval and sends back the public key.

- 4.) This could happen as a direct answer to the wallet's request or by calling the payment provider directly. Today no spec exists that defines how the agent sends its public key.

- 5.) The wallet asks the payment provider to transfers 100 USDC to a specific address for the agent's use.

- 6.) The wallet sends the public key of the agent to the payment provider and registers it with the newly created address.

- 7.) If everything was sucessful, the user gets a notification that the agent is ready to spend the money.

Payment phase (autonomous):

The agent calls a service and receives that is not free and needs to be payed. This could be done by an HTTP 402 response (x402).

- A) The agent sends a payment transaction to the payment provider: "Pay 35 USDC to address Y" The agent signs the transaction with its private key. Today no spec exists that defines how the agent generates its own key pair.

- B) The payment provider uses the agent's public key to verify the signature and sends back a payment proof. The payment backend verifies the signature (by using the agent's public key) and budget, then executes the transfer.

- C) The payment provider informs the agent that the payment was successful.

- D) The user wallet checks the payment agent for any updates and get notified about the payment.

- E) The user receives a notification that the payment was successful.

A critical design decision: the agent generates its own key pair for each wallet relationship. The private key never leaves the agent. Only the public key is shared with the wallet interface and registered on the payment backend. This eliminates the entire class of key-transport security problems — no secret is ever transmitted. Generating a fresh key pair per wallet also limits the blast radius if a key is compromised: only one allowance is affected, not all of the agent's payment relationships.

Note: For agents managing many wallet relationships, Hierarchical Deterministic (HD) keys could offer a practical way to derive per-wallet key pairs from a single master seed — but this is an implementation detail that does not need to be prescribed by the protocol.

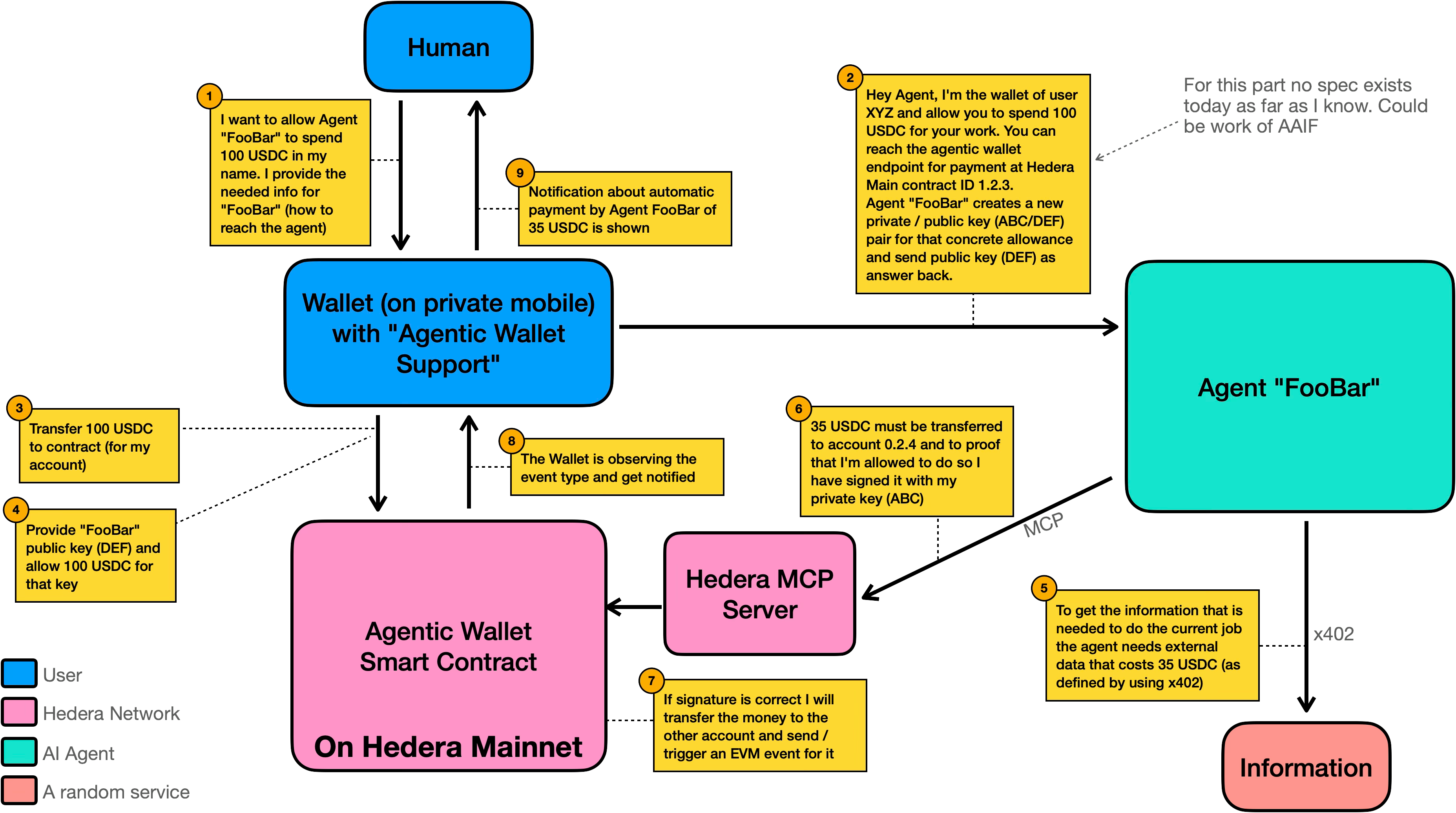

Provider-Agnostic by Design

Every payment that an AI agent triggers in the given idea can be done by an MCP server. Here a payment provider (independent if it is a distributed ledger that allows payment in cryptocurrencies or a classical bank) can provide an MCP server that handles the payment logic. A key property of this architecture: the agent does not need to know what is behind the MCP server. The payment backend can be a smart contract on the Hedera network or a centralized service like Coinbase.

From the agent's perspective, the interface is identical:

- It is requested by a wallet, generates a key pair and provides its public key as part of the response

- It receives a payment endpoint

- It signs payment requests by its private key and sends them to the MCP server

- The MCP server handles the backend-specific logic like calling a transaction on a distributed ledger or calling an API endpoint.

The following diagram shows how the process could like for a distributed ledger as Hedera where a Smart Contract is used to handle the payment logic:

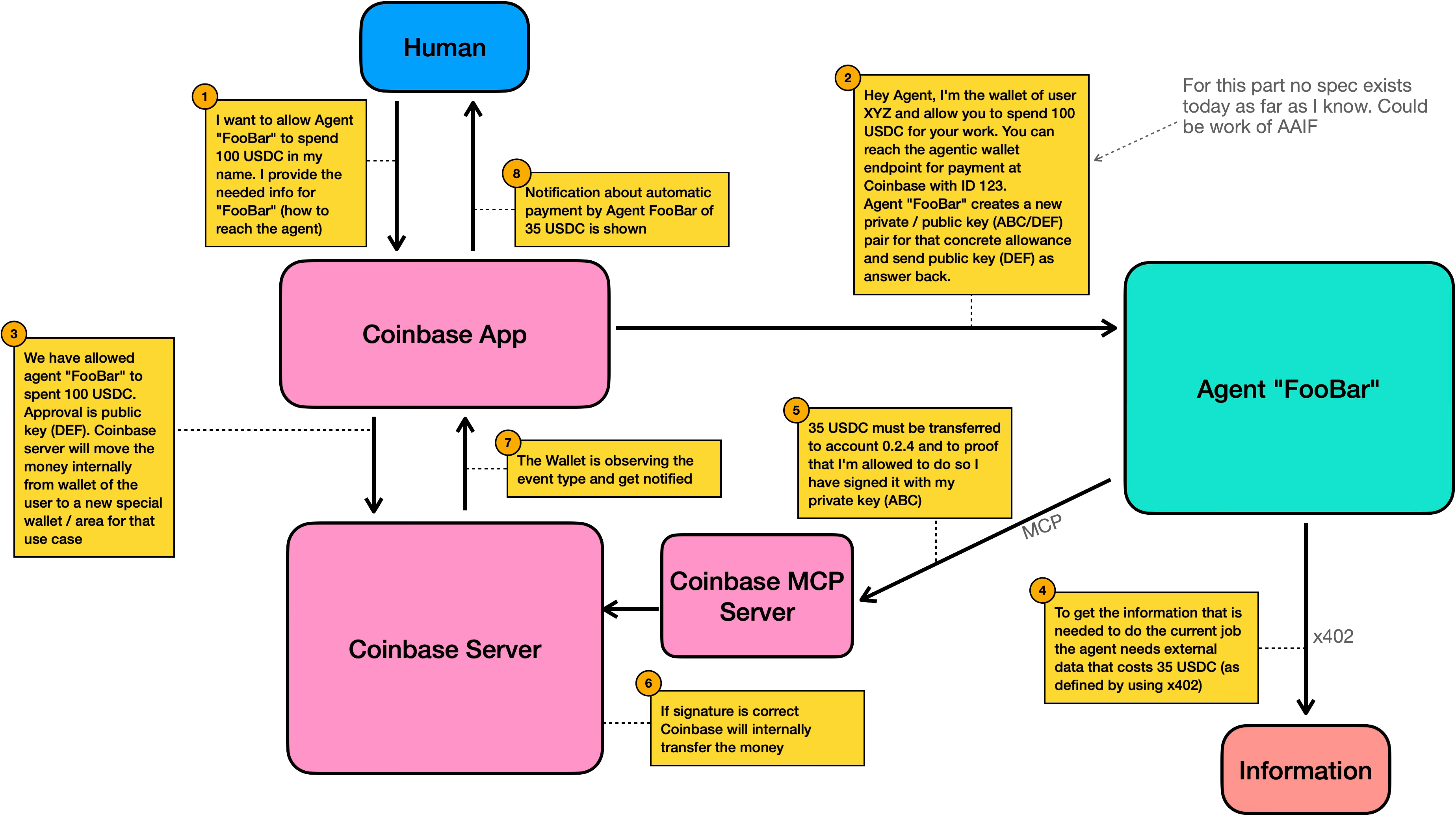

For a centralized payment provider like Coinbase, the flow looks quite similar:

This means the protocol for wallet-agent communication can — and should — be specified independently of the payment backend. Whether the MCP server talks to a Hedera smart contract, a Coinbase API, or a Stripe integration is an implementation detail, not a protocol concern.

What Is Still Missing

This architecture relies on existing specifications (MCP, x402) and established technology (EVM smart contracts, stablecoins). But two critical pieces are not yet defined.

1. Mutual Identity Verification

In the current flow, the wallet app contacts the agent and trusts the response. But how does the wallet know it is talking to the real agent and not an impersonator? If an attacker intercepts the communication and sends their own public key, they receive the spending allowance. Conversely, how does the agent know the wallet request is legitimate? While sharing a public key with a fake wallet is not dangerous by itself, an attacker could potentially direct the agent to work against a malicious payment backend.

The solution is a mutual identity layer: both the wallet and the agent verify each other's identity before exchanging credentials. Specifications for this exist in adjacent domains:

- ERC-8004 provides on-chain identity registries with reputation and validation — already live with 45,000+ registered agents

- A2A Agent Cards provide signed identity and capability declarations

- HCS-14 at the Hiero project of LFDT provides W3C DID-based agent identifiers that work across web2 and web3

But none of these specifications define the specific flow of mutual verification between a wallet and an agent in the context of payment authorization. This needs to be specified. Here the "Agent identity & trust" working group of AAIF would be an ideal place to define this specification, building on the existing identity standards but tailoring it to the wallet-agent use case.

2. Wallet-Agent Credential Provisioning

The communication between wallet and agent — steps 2 through 5 in the flow above — has no specification today.

There is no defined protocol for:

- How a wallet contacts an agent's endpoint and requests its public key

- How an agent responds with credentials in a verifiable way

- How a wallet communicates the payment endpoint and budget constraints back to the agent

Existing approaches address parts of this problem:

- Coinbase's AgentKit, for example, provisions wallet access to agents via API keys and environment variables — pragmatic, but tied to Coinbase and not portable.

- AP2 defines a Credential Provider role that manages tokenized payment credentials, but only for card networks.

None of these provide an open, provider-agnostic specification for the complete wallet-to-agent credential provisioning flow. The protocol that is needed here must be as agnostic as possible to the payment backend. Next to that topics like post quantum cryptography and zero-knowledge proofs are important to consider in the design of the protocol to ensure it is future-proof. The "Agentic commerce" working group of AAIF looks like a good place to start working on a specification for this.

Call to Action

The architecture I have described can work today. Mayn parts of it already exist in the open. The important next step is to define the pieces that are missing in an open, transparent, secure and provider-agnostic way. For me that are natural tasks for the Agentic AI Foundation (AAIF).

The building blocks are here. The specifications are converging. What we need now is the connective tissue that ties them together.

AI agents will need wallets — and those wallets will need a standard way to talk to agents. Let's try to build a open standard that can be used by all agents and wallets.